Step 2: Get honest with yourself

How well did you do in using your income (earnings) to build wealth?

For the sake of illustration, let’s assume you earned $1,000,000 cumulatively over the last 10 years. Now, let’s assume the “growth” number you calculated was $100,000. You can use those numbers to calculate what percentage of your income you retained for the future or used to boost your wealth

Take the $100,000 of “growth” and divide by the $1,000,000 of income = 10 percent

Let’s call that 10 percent your personal wealth retention ratio.

How do you feel about your number? Does it make you proud or does it make you feel you could be more intentional about building wealth?

Now, understand that I don’t expect you to have a ridiculously high wealth-retention ratio. Let’s assume one-third of your earnings will go to taxes and benefits, then you have discretion over the remaining two-thirds of your earnings. You have a choice on what you do with what’s left. You decide on how much you spend on housing, transportation, eating out, and entertainment. These choices can eat up the full two-thirds of the earnings you control, or you can intentionally leave yourself room to save and invest for the future.

So, are you being deliberate about how much of your income you are saving and investing for the future? Are you engaging in wealth-building financial behaviors? Do you want to see that net worth number grow over time? What kind of difference would it make in your life, in the lives of your children or family members, or in the impact of your favorite charities?

Write down your answers to these questions as you reflect.

Step 3: Set goals and go be intentional

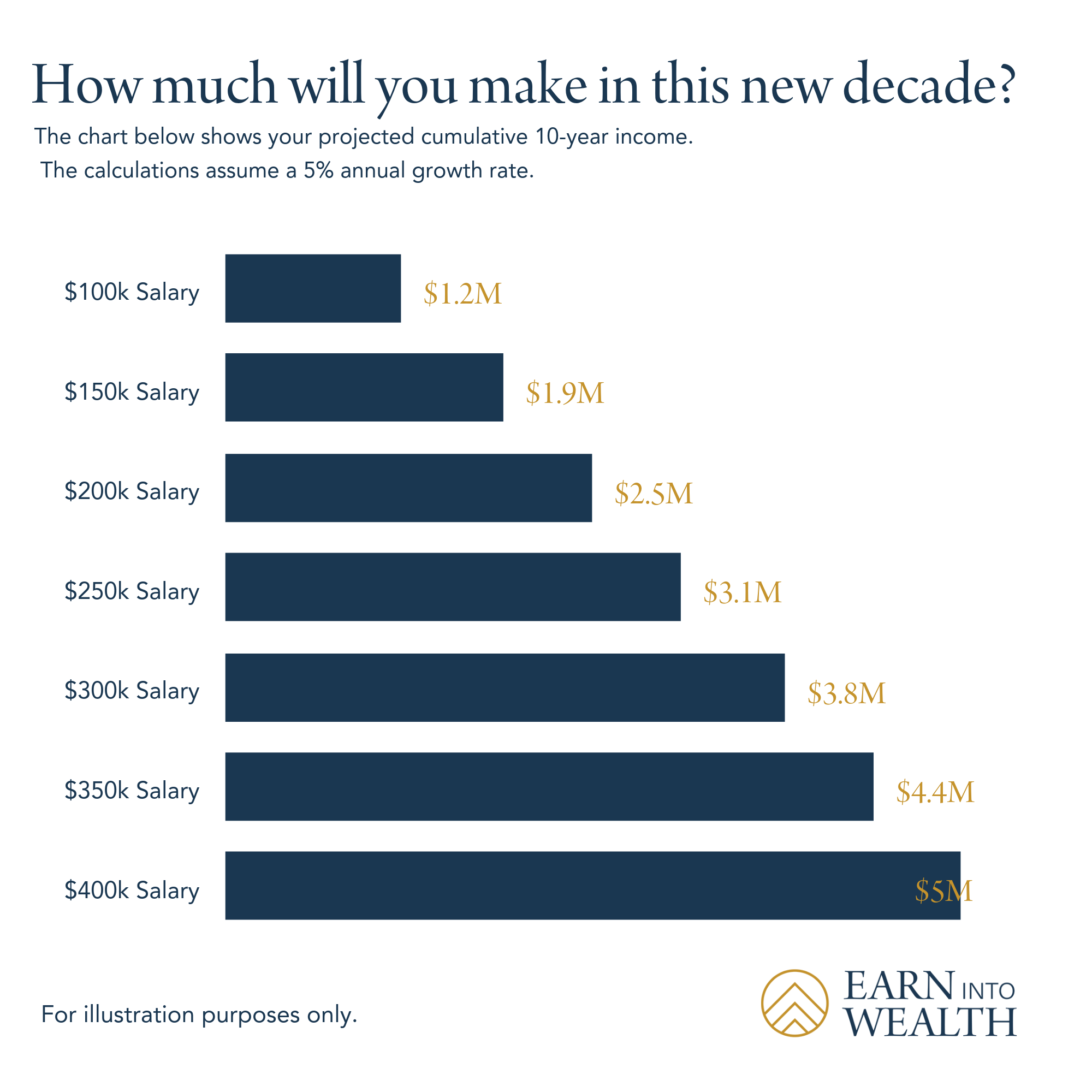

How much are you projected to make over the next 10 years?

To help visualize how to apply your personal wealth retention ratio and how it could make a major impact on your life and your future, let’s review an example. The chart below shows total 10-year income, glimpsed at different income levels. The numbers assume a simplistic growth rate of 5 percent, meaning income is growing by that much each year. While it is rare for income to grow in a straight line, because of course job changes, promotions, and layoffs do happen, let’s keep things simple for the purpose of this projection exercise.

Take a look at the chart and pinpoint where your income falls. Once you know what you project to earn over the next 10 years, hold on to that number as we keep moving to set your goals.

How much of this income do you intend to keep for yourself?

Assuming you have complete discretion over two-thirds of your earnings, how much will you spend on living in the present, and how much will you invest for the future?

To use a salary example from the chart above, if you begin with a starting salary of $150k you’ll earn $1.9M, and have discretion over $1.2M during that time-frame.

Now decide what you want to have left. Some of those costs may be fixed at the moment, such as a mortgage on property you own or lingering debt from school or spending. But as time goes on, you can take into consideration the discretionary choices you make: luxury cars, electronics, or clothing, or more mid-range prices? Do you prefer to spend earnings on travel, or entertainment, and how do you make wise choices in those and other categories of your spending?

It comes down to asking yourself this question: What amount or percentage will go toward growing your wealth and increasing your net worth? Growing your wealth will take your earnings well into the future – making them work for you long after an in-the-moment purchase or idea.

Once you have your percentage or amount of earnings you’d like to invest in growing your wealth, it’s time to move on to the next conversation.